ICICI

CIB

Corporate Internet Banking SAAS

Project

Overview

Corporate Internet Banking (CIB) is a specialized online banking platform tailored for businesses, organizations, and institutions (non-individual customers)

It enables companies from small enterprises to large corporations to access, manage, and transact on their business accounts securely over the internet, 24/7

Supports initiator–approver workflows (one user initiates, another approves payments), audit trails, role-based access, 2-factor authentication, and transaction limits for robust security.

Difference between Corporate & Retail Internet Banking

Corporate Internet Banking

001 Commercial firms for business purposes

002 Employees share the same account ID and password

003 Transactions require approval workflows to keep corporate funds in check

Retail Internet Banking

001 Individuals for regular, day-to-day transactions

002 Every customer has a different ID and password

003 Does not need any approval as only a single individual tracks their funds

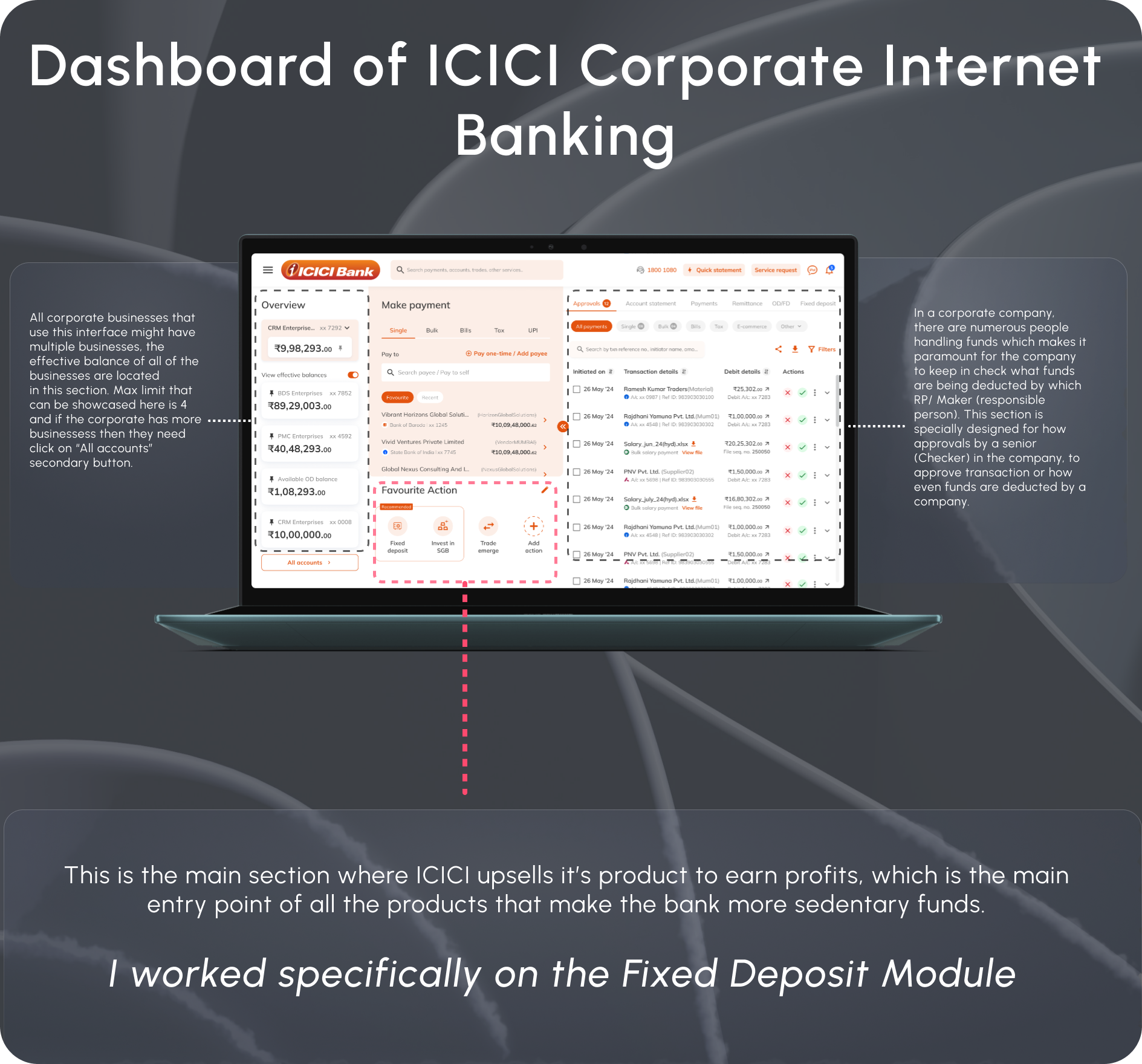

ICICI Corporate Internet Banking (CIB)

Designing high-stakes financial workflows for enterprise users

Improved clarity and decision-making across Fixed Deposit (FD) creation, approval, and closure flows in a complex multi-user banking system.

Key Modules &

Impact

Worked across multiple high-stakes financial workflows within ICICI Corporate Internet Banking (CIB), focusing on improving clarity, efficiency, and business outcomes.

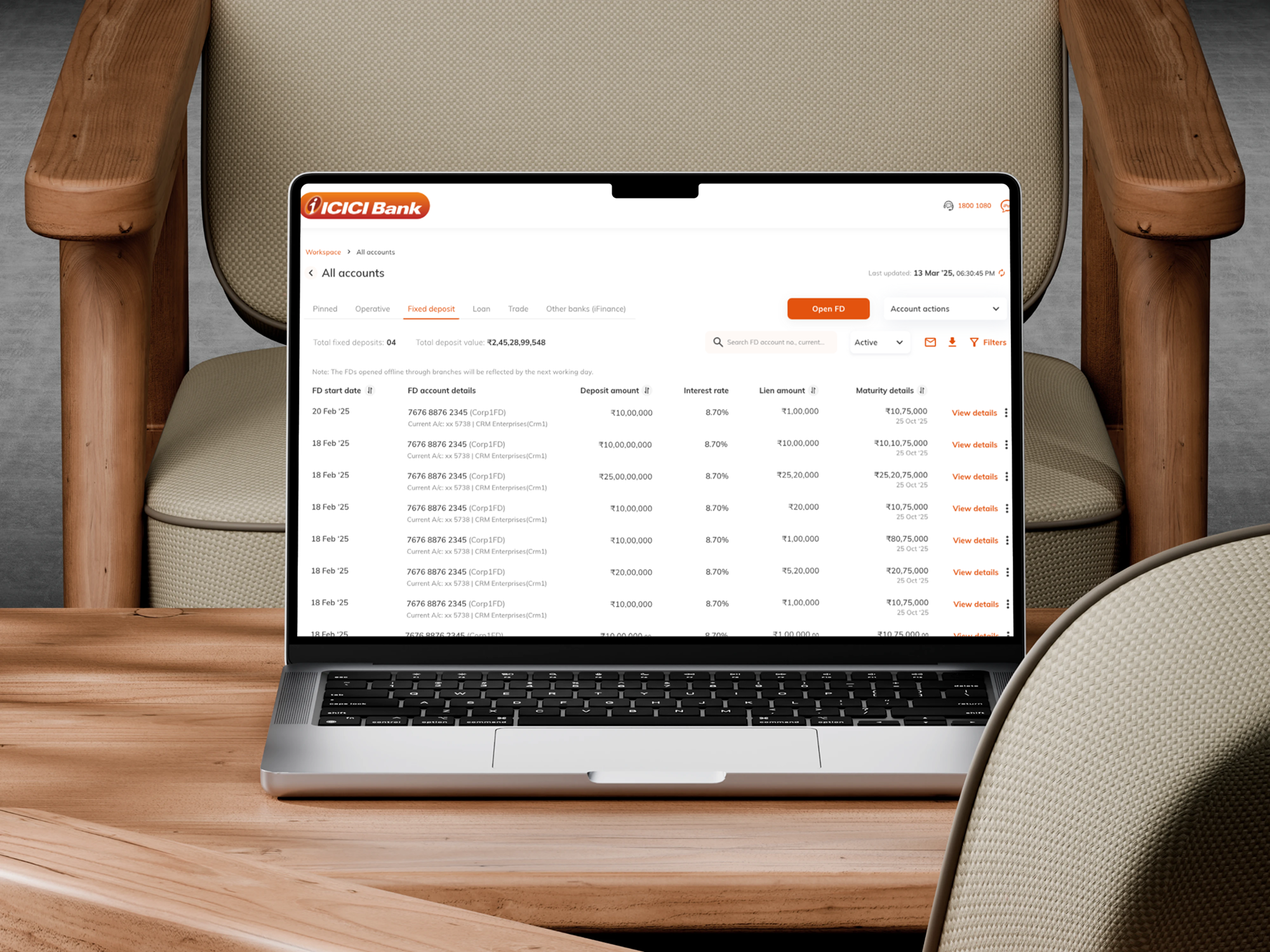

Fixed Deposit (FD) Creation -Maker Flow

Designed a structured, step-by-step flow to reduce ambiguity and prevent high-value input errors, improving clarity in transaction initiation.

FD Approval - Maker–Checker / Checker Flow

Simplified multi-user approval workflows by clearly defining task ownership and status visibility, enabling faster and more confident decision-making.

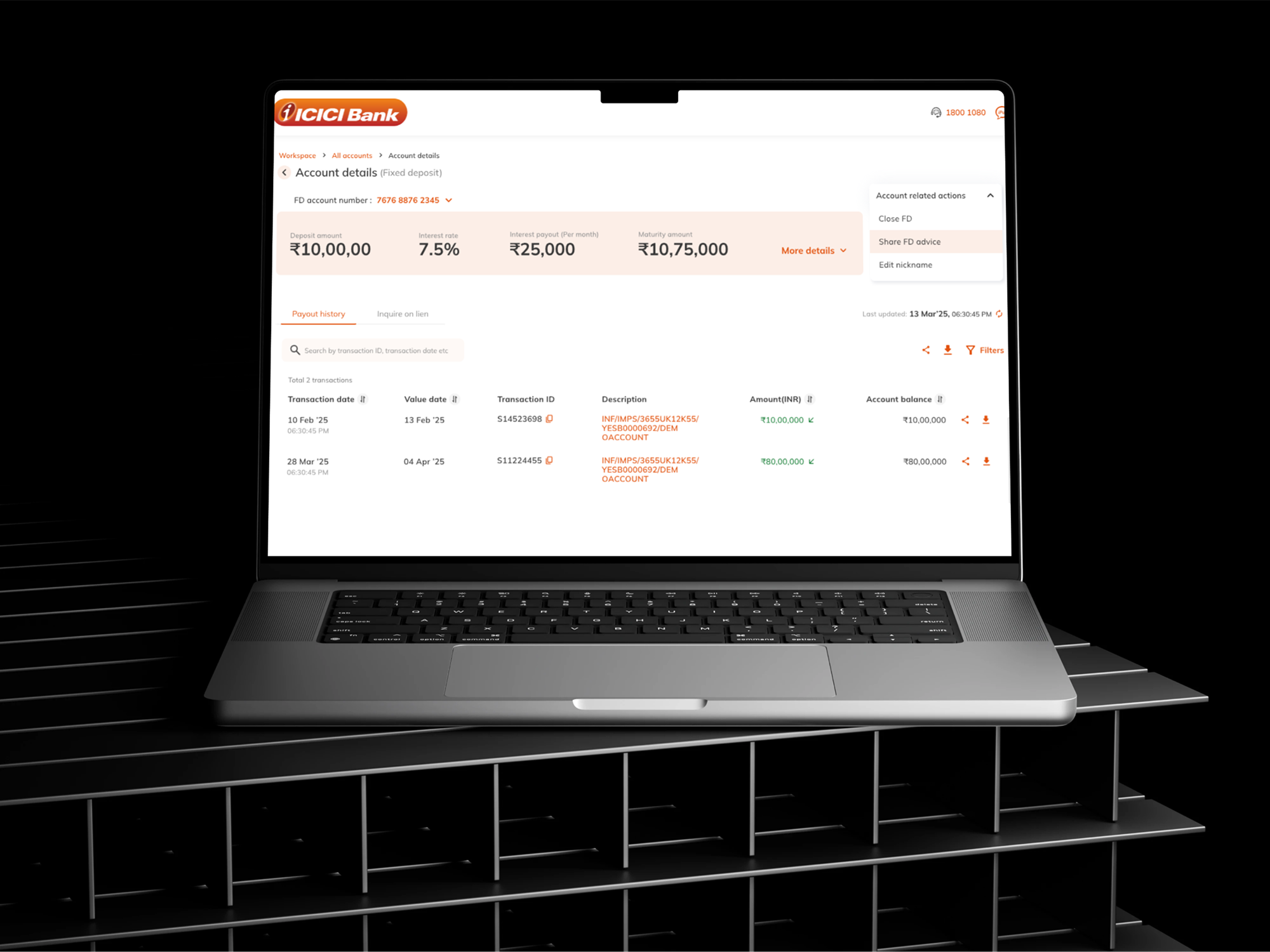

FD Closure - Maker Flow

Redesigned closure journeys to reduce friction and guide users through critical financial decisions with better clarity and control.

FD Closure Approval - Multi-role Flow

Improved approval visibility and reduced confusion in closure workflows across different user roles.

Cross-Sell: Overdraft (OD) against FD

Introduced a decision layer during FD closure to offer OD as an alternative, enabling banks to retain funds and support revenue growth.

OD Journey (RBI Compliant Design)

Iterated 13+ times to design a compliant OD experience aligned with RBI guidelines, balancing regulatory constraints with usability.

Fixed Deposits are one of the most fundamental yet high-impact financial products in corporate banking making their usability critical to both user success and business outcomes.

Understanding Corporate FDs

Fixed Deposits (FDs) are a core financial product that allow businesses to invest surplus funds for a fixed tenure in exchange for guaranteed returns.

In a corporate banking context, FDs are not just savings instruments, they are part of a broader treasury strategy, where enterprises manage liquidity, optimize returns, and balance risk across financial instruments.

Unlike retail FDs, corporate FDs involve higher transaction values, multi-level approvals, and integration with other financial services such as overdrafts and credit facilities.

Generating Revenue

Fixed Deposits play a critical role in a bank's financial ecosystem. Deposited funds are utilized by banks to lend at higher interest rates, creating a margin between borrowing and lending, making FDs a key contributor to revenue generation.

In corporate banking, higher deposit values and longer tenures make FDs especially valuable, not only for revenue but also for strengthening long-term customer relationships.

Additionally, FDs act as a gateway for cross-selling financial products such as loans, overdrafts against deposits, and treasury services further increasing customer lifetime value.

Designing the Experience

As a UX Designer working on ICICI Corporate Internet Banking (CIB), I was responsible for improving the end-to-end Fixed Deposit booking experience within a complex enterprise environment.

My work involved identifying usability challenges in the existing flow, restructuring the experience to reduce cognitive load, and introducing decision-support mechanisms such as real-time financial feedback and guided inputs.

I collaborated with cross-functional teams to ensure that the redesigned experience aligned with both user needs and business objectives, particularly around improving discoverability, conversion, and product adoption.

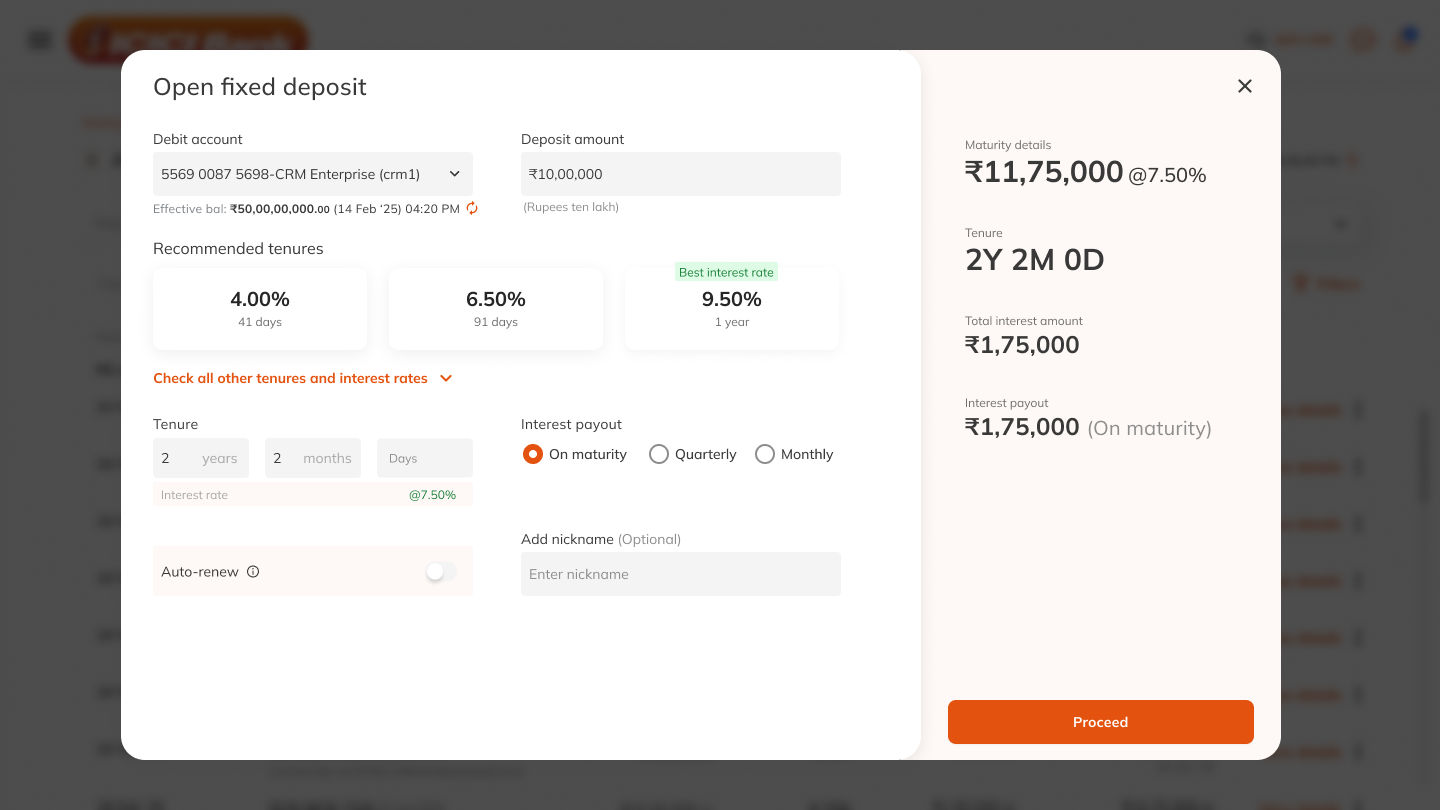

Transforming Fixed Deposit Booking Experience

From a complex, form-heavy workflow to a guided, insight-driven investment experience

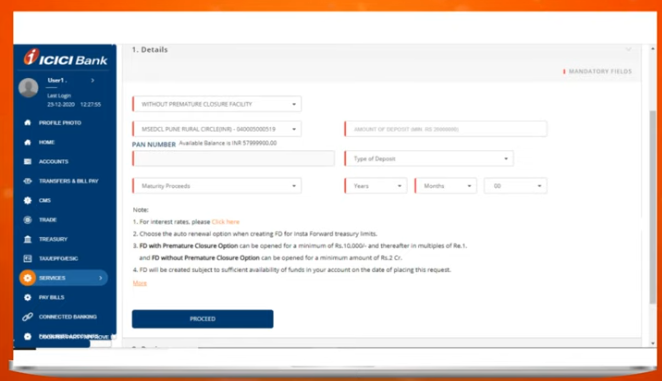

Before

A fragmented, form-heavy interface that required users to manually interpret financial inputs, leading to high cognitive load and decision uncertainty

Key issues

- - Overloaded form with multiple fields and unclear hierarchy

- - No real-time feedback on returns or maturity value

- - Critical inputs (tenure, interest type) lacked guidance

- - Decision-making required external calculation or prior knowledge

- - Poor visibility of outcomes → low user confidence

After

A guided, user-centric flow that simplifies decision-making through contextual insights and real-time financial feedback

Key improvements

- - Structured layout with clear grouping and progressive input flow

- - Real-time maturity value and interest breakdown displayed upfront

- - Recommended tenure options to support faster decisions

- - Integrated financial feedback → no need for external calculation

- - Improved clarity and trust through transparent outcomes

Process

A structured, stepped approach to bring clarity to the Corporate Internet Banking ecosystem.

Discovery

We begin by uncovering the core business needs, conducting thorough user research, and establishing a robust design system to define the visual blueprint.

Research - Branding - Design System

Design

Translating findings into tangible interfaces. We formulate user journeys, architect the information structure, and craft high-fidelity website designs.

User Experience - UI / IA

Delivery

Finalizing the solution and handing it over to the development team, while incorporating active feedback for rolling iterations.

Delivery To ICICI Team

Context of Fixed Deposits in CIB

Before just showcasing just the designs let's give you more context on how fixed deposit are actually transacted for corporate business and how banks offer that

User Personas

There are 3 user personas that are to be specially noted in Corporate Internet Banking

MAKER

- + I am limited to the extent I can tackle the funds of an organisation.

- + I can initiate payments or other non-financial request in an organisation but I cannot approve payment request made by others.

- + As I am the maker of the request, my request has to go through a series of approvals before the funds are deducted from the business account.

MAKER+

CHECKER

- + I am NOT limited to the extent I can tackle the funds of an organisation. Though I am the working class of the company and still have to keep check and generate request, I am considered lower in rank than pure checker.

- + I can initiate payments or other non-financial request in an organisation and I can as well approve payment request made by others.

- + As I can be the maker of the request, my request has to go through a series of approvals by other Maker+Checker/Checker before the funds are deducted from the business account.

PURE

CHECKER

- + I am NOT limited to the extent I can tackle the funds of an organisation.

- + I don't initiate payments or other non-financial request in an organisation as I am on the upper management level and I can as well approve payment request made by others.

- + I don't initiate any requests. I am not the Maker in any scenario, I am only the Checker.

Case Scoping

These 3 personas are inter-related in the following ways in FD creation ecosystem

Edge cases in User Personas

Sole Proprietor companies only have one user persona

In case the Maker is a sole proprietor of the company (No approval process)

In case the Maker is a sole proprietor of the company (No approval process)

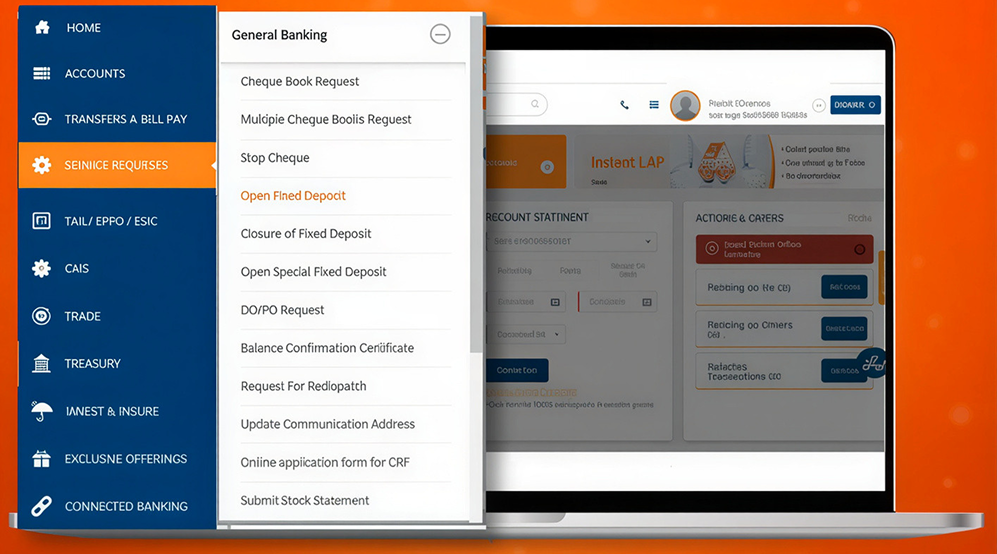

Key Experience Gaps in FD Booking Flow

Low Product Visibility

01Why this matters

Critical financial actions like Fixed Deposit booking were buried within navigation, making discovery difficult for users.

- - Users struggled to locate FD features within the system

- - High-intent users dropped off before even initiating the journey

- - Reduced product discoverability directly impacted adoption

- - Poor visibility of outcomes -> low user confidence

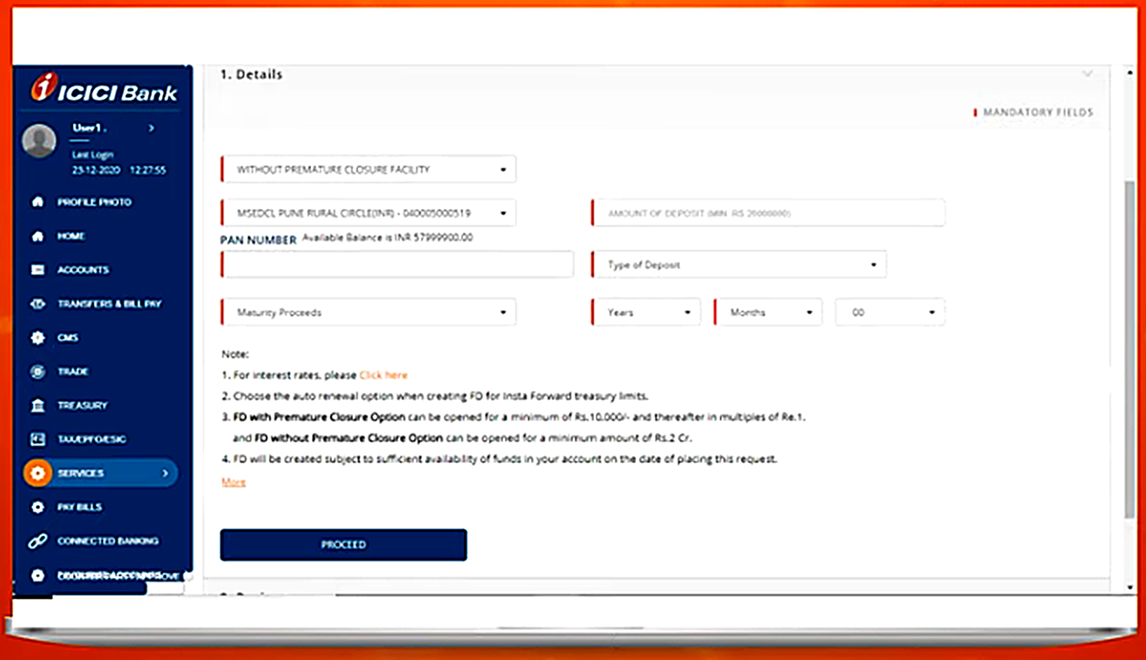

Fragmented Information Hierarchy & lack of upselling

02Key issues

The interface lacked a clear structure, forcing users to process dense financial inputs without guidance

- - Critical inputs (tenure, interest type) was missing

- - Poor visibility of outcomes -> low user confidence

- - Asking for premature closure facility too early in the form, even before user has decided whether to go forward with the FD opening

- - No way introduced to nudge the user to increase the ticket size of Deposit amount of FD

- - No real-time feedback on returns or maturity value

- - No provision introduced to enter Maturity date instead of just tenure

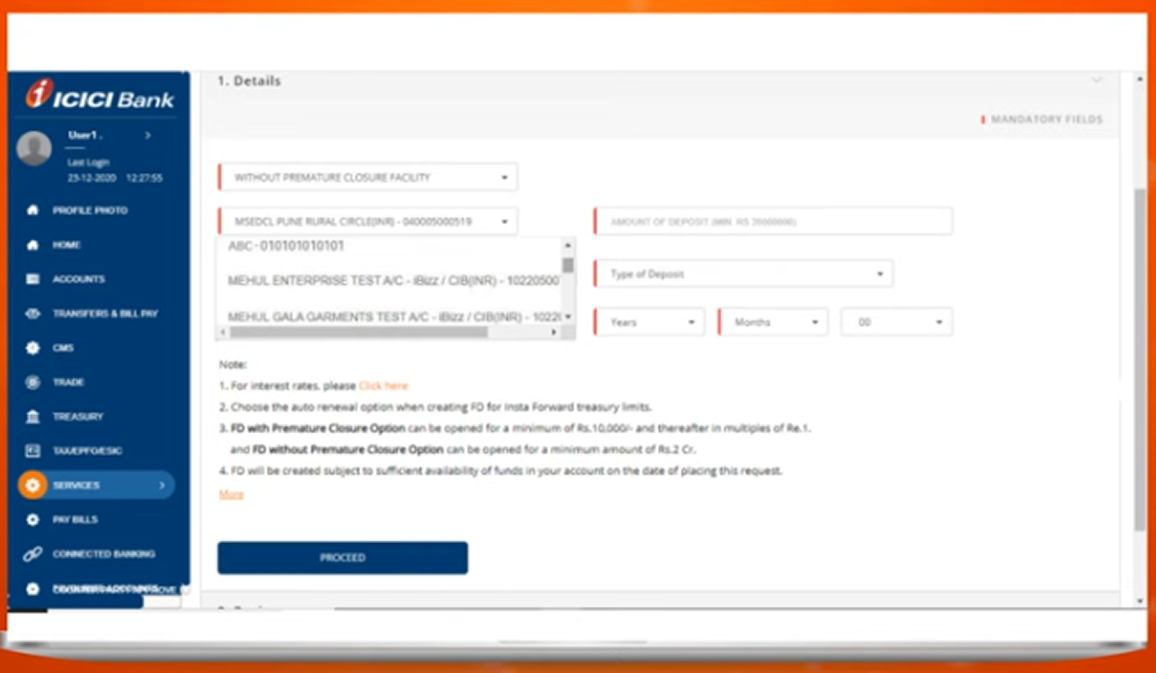

Decision Paralysis in a Complex Flow

03Key issues

Users were required to make financial decisions without sufficient support, leading to hesitation and drop-offs

- - As the dropdown of choosing an account was highly scrollable and without complete information about the account, users got stuck in choosing

- - Heavy reliance on prior financial knowledge or external calculation

- - Lack of guidance on higher interest rates on higher deposit amount or longer tenure gave no encouragement to the user to increase ticket size of FD deposit amount

Impact on FD Ecosystem The experience was not just inefficient, it actively discouraged users from completing high-value financial actions.

(Barrier to Entry)

High

Users struggled to even discover FD options, limiting initial engagement.

(Journey Friction)

70%

of users bounced off at first step due to poor form structure causing decision paralysis.

(Successful Conversion)

5%

converted due to unclear guidance on maturity proceed and interest rate.

(Ticket Size)

Low

amounts defaulted to because there was no upfront upselling techniques incorporated.